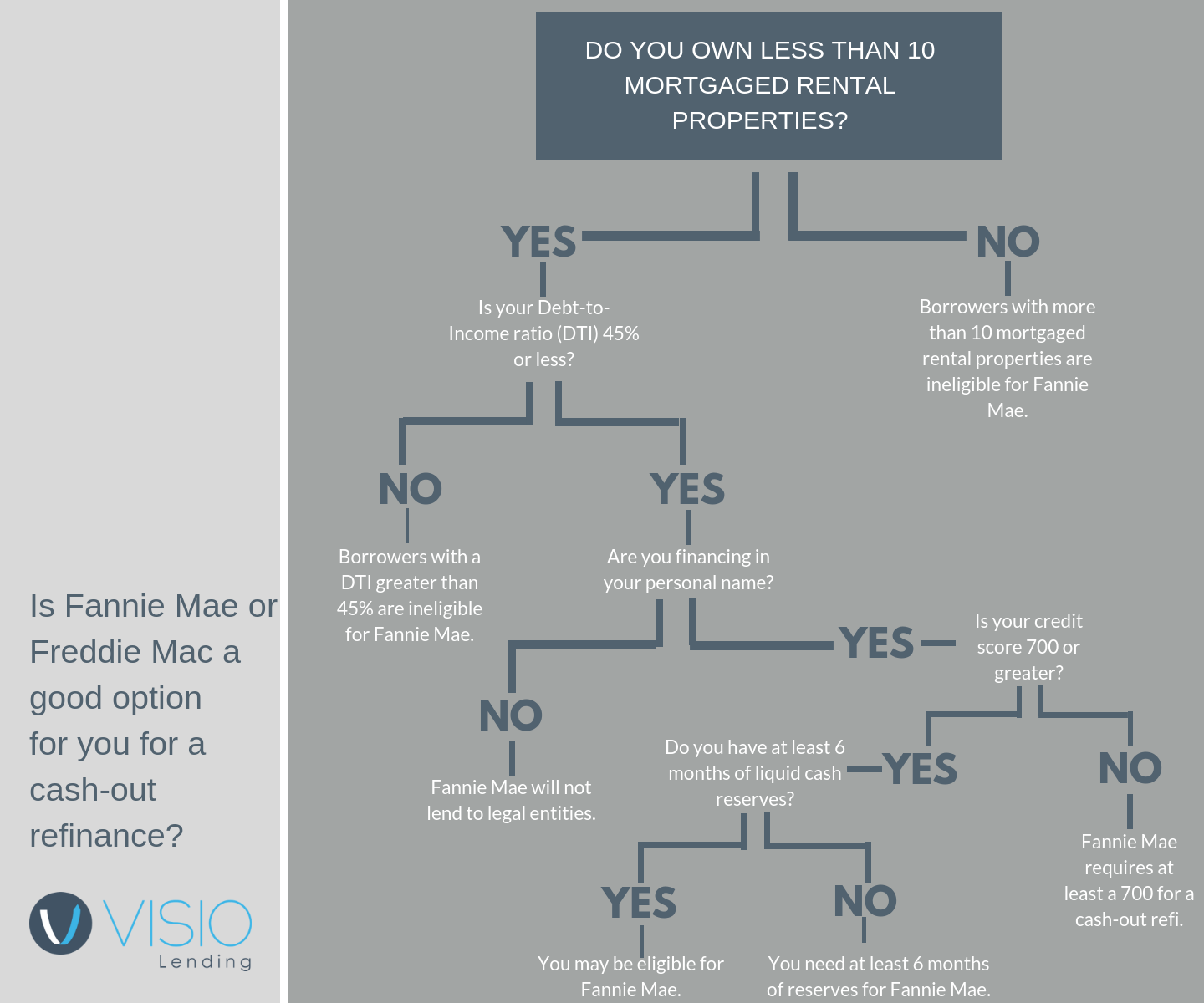

While government sponsored loan programs (Fannie Mae and Freddie Mac), tend to be the most affordable, they also have the most restrictions. Savvy investors looking to build wealth and grow their rental portfolios often are unable to qualify for these loans. Visio, on the other hand, has loan programs tailored to residential real estate investors, which includes low documentation (no tax returns!). We’ve done a side by side comparison of our qualifications for purchases versus Fannie and Freddie:

Minimum Credit Score

Fannie/Freddie: 640, which is only acceptable when your LTV is less than 75% AND you have 12 months of liquid cash reserves

Visio: 680 with an LTV of 80% or less

Maximum Number of Mortgaged Rental Properties

Fannie/Freddie: 10

Visio: No limit

Minimum Number of Liquid Cash Reserves

Fannie/Freddie: 6-12 months, depending on your Debt-to-Income

Visio: We require 6 months of Principal, Interest, Taxes, Insurance and Association Dues (PITIA)

Maximum Debt-to-Income Ratio (DTI):

Fannie/Freddie: 45%, if you have 12 months of financial reserves

36%, if you have 6 months of financial reserves

Visio Lending: Instead of DTI, we use DSCR, which evaluates property cash flow rather than personal income. We will not look at your tax statements or your personal income verification.

Another key differentiator of Visio Lending is that we loan to corporate entities (LLCs) in addition to individuals. Want more guidance on when government financing is a good option for you? Check out our Decision Tree. Want more resources for landlords? Visit our Resources Page.

Editor's Note: This post was originally published in December 2018 and has been updated in July 2020 for freshness and accuracy.

{kind=link}